Two truths and a lie about debt

Venture debt, income sharing, and victory laps

People are talking about debt this week. At Wharton, I got an A in Financial Derivatives but got rejected from the Financial Engineering course, so I know enough about this stuff to explain it but not enough to do real damage to the economy. There are hundreds of (though probably not that many more) counterfactual carbon copies of me, who did get into financial engineering and now get their intellectual stimulation from inventing new financial structures or terms and general gamesmanship; the money is honestly secondary to the bragging rights.

The “tech Twitter consensus” this week is that investments in startups structured as debt are good and investments in students structured as debt are bad. Is that true?

Securitizing startups as a service

Alex Danco wrote a post, arguing that debt would replace equity as the preferred funding mechanism for some startups. The TLDR: more startups today have recurring revenue (e.g. every B2B startup…), so taking on debt financing, securitized against that future recurring revenue and the underlying IP of the company, can result in better outcomes for the startups and for the creditors extending credit. It’s a pretty good piece, so I won’t rehash the pros/cons of debt and equity too much.

For traditional fixed income investors, startup debt mainly offers a higher-risk, higher-return offering than typical corporate bonds. For VC’s, it’s more adapt or die -- they have money and their investors expect that money to be invested. Of course, plenty of VC/PE investors are not making those investments today, and honestly, I am very envious of their business model: collect 2% yearly management fees, sit on an Aruban beach, do not take calls.

Danco argues,

[I]magine how much investor interest you could get in a diverse basket of recurring revenue from, say, 10 different startups that’ve all raised from Tier 1 VCs. People talk about how great it would be to invest in a unicorn basket; this would probably be even better. In some ways this is threatening to VCs, since it’s competing capital; but it also reinforces their importance as curators and underwriters.

The risk to VCs isn’t that their role disappears. It’s that once this happens, the muscle memory for how to structure funds and term sheets immediately goes out of date. VC firms should spend time today thinking about how they’re going to prepare for this new world, in case it comes true.

There’s a lot to unpack here, I want to focus on the potential impact on the venture capital industry and on the technical financial engineering.

Venture capital employees typically have two key roles: “valuation” and “relationships.” Valuations are typically done by 25 year old analysts “building” Excel workbooks on Adderall and relationships are typically managed by the 40 year old managing directors. Occasionally the analysts cold-call founders or find bottles of wine. And sometimes seed investors skip the Excel step, which is how you end up with insane decks, with “Monte Carlo simulations” which somehow turn tiny startups into having more revenue than the GDP of Aruba.

One funny aspect of debt is that its consistent recurring revenue is relatively easier than valuing equity. In a world where more VC investments are done in debt form, even more investors can skip the Excel monkeys and focus only on the relationships (losing the “muscle memory”). If the value-add of a VC is only the network, it means that individual well-connected VC’s now have more power; you’d likely see a lot more VC’s open up small boutiques and organize these deals, just as solo investment bankers have disintermediated their businesses, e.g. in IPO advice.

Another funny aspect of corporate debt is that, because debt involves contracts and papers and things you can estimate, it is fairly rare to not hedge debt positions. For all Elon Musk rails on short sellers, it is very typical for holders of corporate convertible debt to short the underlying stock to hedge the associated credit risk. “Short selling should be illegal,” says the man who has $13 billion in debt outstanding to creditors who have shorted his stock (“jerks who want us to die”). If you couldn’t short sell Tesla Tesla would also find far fewer lenders and/or higher interest rates.

My own take is that a lot of the SaaS startups are actually just selling to each other (looking at you, Y Combinator) and their credit risk is actually very correlated, so investing in a “unicorn bucket” is not what you want! I guess you diversify your single company risk but you hold a ton of “SV startup” risk, and if you think that’s uncorrelated with the rest of your portfolio, fine, but I don’t think that’s what most people are thinking about.

So then how do you hedge startup debt, with both equity and credit risk? It’s going to be more expensive, startups are weird and unpredictable, and the typical instruments are out (shorting the stock) so you should expect to pay a counterparty a lot more for a credit default swap - a “side bet” where the issuer pays the buyer if the company goes into default. The company is usually not involved, unless it is.

Maybe equity holders, or prospective investors, will write the CDS? You are entering essentially a capped synthetic long position, where you earn money if the company pays off its bonds and you lose money if the company defaults. It’s also convenient that the CDS doesn’t involve the actual company itself; since companies in this new world might take less money, they might also have fewer investors in each round. If an investment firm can’t get allocation for a given round, they can still sell CDS and get long exposure!

Alex Taussig replied to the Danco article with a take on the debt-equity agency problem.

The wonderful thing about equity is that it aligns incentives. Debt tends to do the opposite. Debt holders get paid even if the business is floundering. They do have an incentive to keep the company alive, so that they can continue to earn a yield, but they will also be the first ones out the door when something dramatic changes.

The classic example of the agency problem is that you have a company which has a bunch of debt and is in a bad state. A very simple example:

Company has $1M in outstanding debt due in a year

Project A: returns $10M in a year with 50% probability, $0 with 50% probability

Project B: returns $1.5M in a year with 100% probability.

Debt has a preferred claim on a company’s cash flow compared to equity, so the debtors will very heavily prefer project B over project A, because the expected value of project A is $0.5M, and the expected value of project B is $1M. However, the equity holders (and presumably company management) would prefer project A, which has a $4.5M expected value, versus $0.5M expected value for project B.

One solution is, “don’t go into financial distress.” The other is, “don’t take debt if you’re not set up with cash flow to manage that debt.” But I’d argue that equity comes with similar strings attached; you could just as easily say, “don’t take equity investments if you’re not able to take the appropriate level of risk associated with those investments.”

Securitizing students as a service

Lambda School is a “college disruptor” which puts students through essentially a software engineering bootcamp, for zero upfront cost, in exchange for an “income share arrangement” (ISA), where the students pay a percentage of their income to Lambda, with certain caps/floors attached to it. The pitch is that the ISA’s align student and Lambda incentives, because Lambda makes more if the student makes more. But what happens if Lambda takes out loans, securitized against those ISA’s?

Lambda and their CEO are already, shall we say, controversial, and they’re working with a company run by the “grandfather of collateralized debt obligations,” which you might remember from such movies as The Big Short. So the optics are definitely pretty bad.

But I’m really not convinced that these ISA resale arrangements are “bad.” Modern financial engineering is all about slicing risk and reselling it. And yes, oftentimes people misprice that risk and sometimes people straight up lie about the risks. The credit rating agencies were in the lying category, and I’m not going to pretend that people won’t lie about the risk associated with ISA’s now.

Fundamentally, these ISA resales allow these bootcamps to exist. The ISA issuance is like a bond: an upfront payment to Lambda, and deferred payment with “earnings risk,” that students might not earn enough to pay back the targeted yield. This is, like, a normal thing to financialize and sell. Lambda expects future cash flows, but doesn’t have money today, so they should take out a loan and finance current operations. To get better rates on a loan, you should securitize it against your assets, and the most obviously matched asset is the future cash flows from the ISA’s.

The main argument against these arrangements seems to be that by transferring repayment risk to a third-party, Lambda and other issuers are incentivized to pump students through the programs, regardless of program quality:

A marketplace for ISA investors “immediately underscores to me that an ISA is a financial product that is market-driven, and I have no reason to trust that is a one-sided bet in the students’ interest,” says Jessica Thompson, director of policy and planning at the Institute for College Access & Success. “In fact,” she adds, “my fear is that history would tell us that the one-sided bet is probably going in the other direction.”

The argument strikes me as true, but true independent of the ISA securitization. Regular “tuition upfront” bootcamps are just as incentivized to pump students through and game all the metrics to look better. This argument is also true of regular universities. There is a lot of BS in the education industry; the financialization of it is not necessarily the cause.

My pitch is that in the long-term, investors and students will learn which bootcamps are snake oil and no longer invest in those ISA’s. Bad outcomes for students do map to bad outcomes for investors, and you learn or you lose money.

Anyways, everybody does this. Insurance companies used to go to reinsurance companies to mitigate their payout risk; after Hurricane Andrew in 1992 and the failure of eight insurance companies, they tend to sell catastrophe bonds, which pay high interest if nothing happens but pay nothing if natural disasters occur. I generally think cat bonds are “good” for all parties - insurance companies take lower risks, thus offering lower rates to customers, and investors can invest in risk which is (usually) uncorrelated with the market.

If you’re going to get mad at people pitching bad investments to the underinformed, I’d start elsewhere:

(COKE is not the ticker of the Coca-Cola that you’re thinking of).

The upshot

For me, the most interesting aspect of debt as a funding source is that it allows you to build non-moonshot companies. In a world where your only funding options are bootstrapping and venture as funding options, you lose out on a lot of the medium sized-ideas. Not every company needs to grow to a billion (or 10 billion), and those expectations probably kill a lot of value. I’ve written previously about how Patreon is a great product which creates a lot of value for its customers and could be profitable and sustainable with a 5% fee, but has a mandate from its investors to hire lots of engineers/sales/ops and to grow revenue.

Investment firms can also write CDS positions on startups they otherwise wouldn’t have been able to get into. Now you have no more excuses on missing out on the next Stripe - you just have to find Stripe’s debt buyers and offer them a hedge against their debt investment. Come on VC’s, you have to be innovative sometimes too!

Lambda School and other bootcamps would also probably not be able to exist without their securitization and usage of debt. Financial engineering often gets a bad rap, but in its best form, it enables new business models and creates value for others.

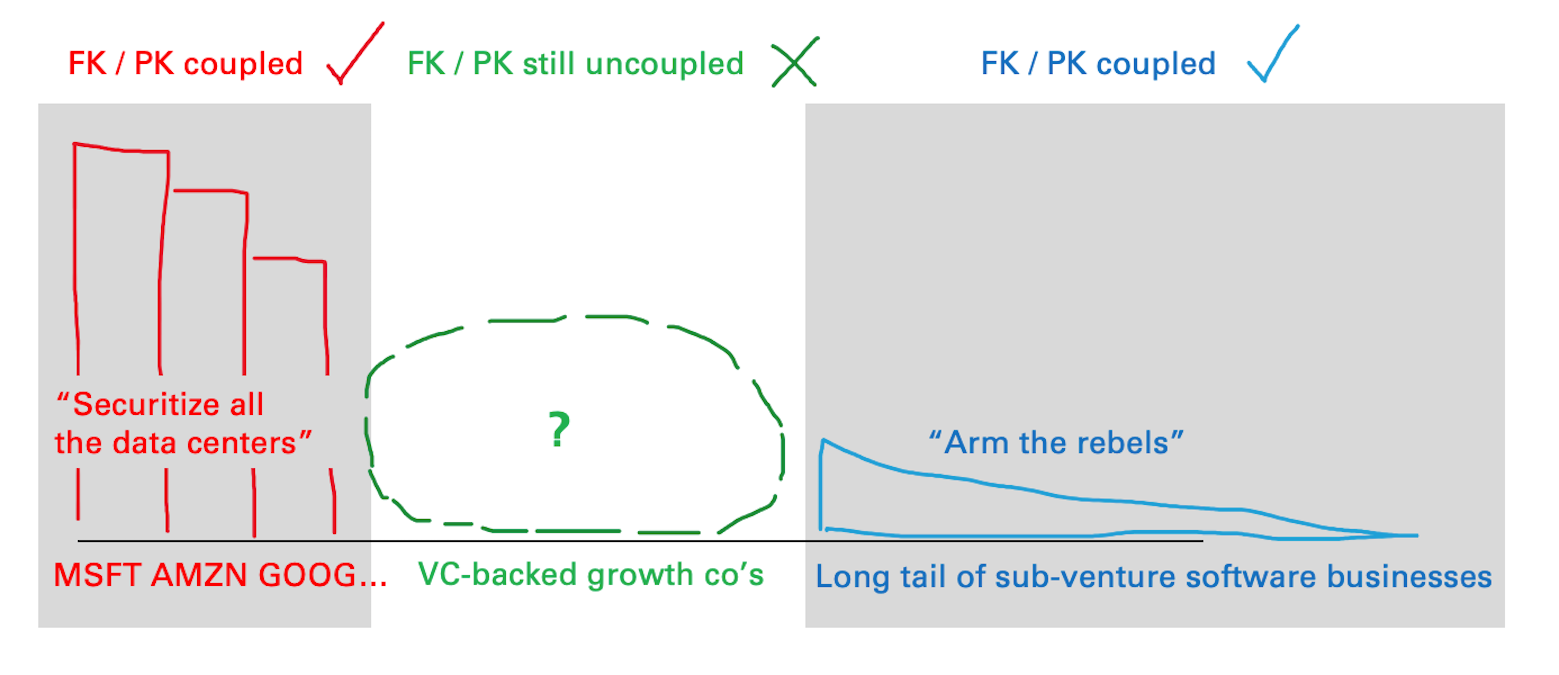

In Danco’s chart (above), we have the long-tail of sub-venture businesses which can take debt and be sustainable in this new model. But in today’s world, a decent number of those businesses took VC money, moved into that middle zone, and represent lost value if/when they die. I’m excited to see more companies stay in that lane and create more sustained value for others.

I hung out recently with a friend who uses Rover to find catsitters, who complained about how bad Rover’s interface was and that the app couldn’t figure out the right price. They eventually had to pay the catsitter directly via Venmo. Rover makes money on a 20% cut of each marketplace transaction, and I guess they made no money off of my friend’s 4 hours of catsitting.

Despite that terrible interface, Rover is gaining market share vs Wag, their Softbank-funded competitor, and raised $155M led by T Rowe Price, a firm which has openly announced their distaste of Softbank’s tactics. I have great respect for T Rowe Price now, they got burned by Softbank/WeWork and are now out for revenge, investing in more capital-efficient competitors to Softbank companies.

Here’s a free investment thesis: make debt investments in startups with cash flow and going up against Softbank-funded companies. Tell them to grow and fast follow the market leaders, but control the cash burn. When the Softbank companies go under from unrealistic growth expectations (or whatever else), step in as a drop-in replacement.

Shameless bragging

I say a lot of dumb shit on the internet, so I have to celebrate the times when I’m right. This week:

Me, October 2019: “Zume Pizza is #deadpool”. Bloomberg, February 2020: “Inside the mass firings at Zume, one of Masayoshi Son’s latest investment debacles.”

Me, Feb 3, 2020: “The Iowa caucus app should have been a Google Form.”

538, Feb 13, 2020: Nevada Democrats Say They’ll Replace Their Caucus App With iPads And A Google Form

Please do not reply with times I’ve been wrong.

Coda

Header image from www.distel.co, it looked more interesting than a derivatives textbook. Memes from the best account on Instagram, but I couldn’t find a mezzanine finance one.

What did you think of this post? I’m trying different newsletter formats (more on that in the near future), and need your feedback! Leave a comment on Substack.